Did you know that even if the tax bill sitting on your desk is clearly incorrect, IRAS still expects you to pay the full amount within one month? It feels counterintuitive, and for a growing Singapore SME, that sudden hit to your cash flow can be genuinely stressful. You might feel anxious about penalties or simply confused by a complex computation that doesn’t seem to align with your actual bookkeeping records. We understand that managing statutory regulations is daunting, but you don’t have to face these financial hurdles alone.

This guide will show you exactly how to file a tax objection with IRAS to correct these errors while ensuring your business remains fully compliant with the latest 2026 regulations. By mastering this process, you can protect your company’s cash flow and secure a successful revision of your tax bill. We’ll walk you through the digital filing steps on myTax Portal, explain the critical two-month deadline for companies, and clarify how to handle the “pay first, object later” rule without risking unnecessary penalties. Understanding your rights as a taxpayer is the first step toward a more secure and predictable financial future for your business.

Key Takeaways

- Understand the strict timelines for your submission, specifically the two-month window for companies and 30 days for individuals following the date on your Notice of Assessment.

- Learn how to file a tax objection with IRAS efficiently by using the myTax Portal digital service to ensure your request is lodged correctly and processed without delay.

- Navigate the “pay first, object later” policy to avoid an immediate 5% penalty, ensuring your company remains compliant while you challenge an incorrect assessment.

- Identify the essential supporting documents, such as tax computations and bank statements, required to provide clear and valid grounds for a successful revision.

- Discover how a well-prepared objection protects your business’s cash flow and ensures your final tax liability aligns accurately with your actual bookkeeping records.

Understanding the IRAS Notice of Assessment (NOA) and Objection Deadlines

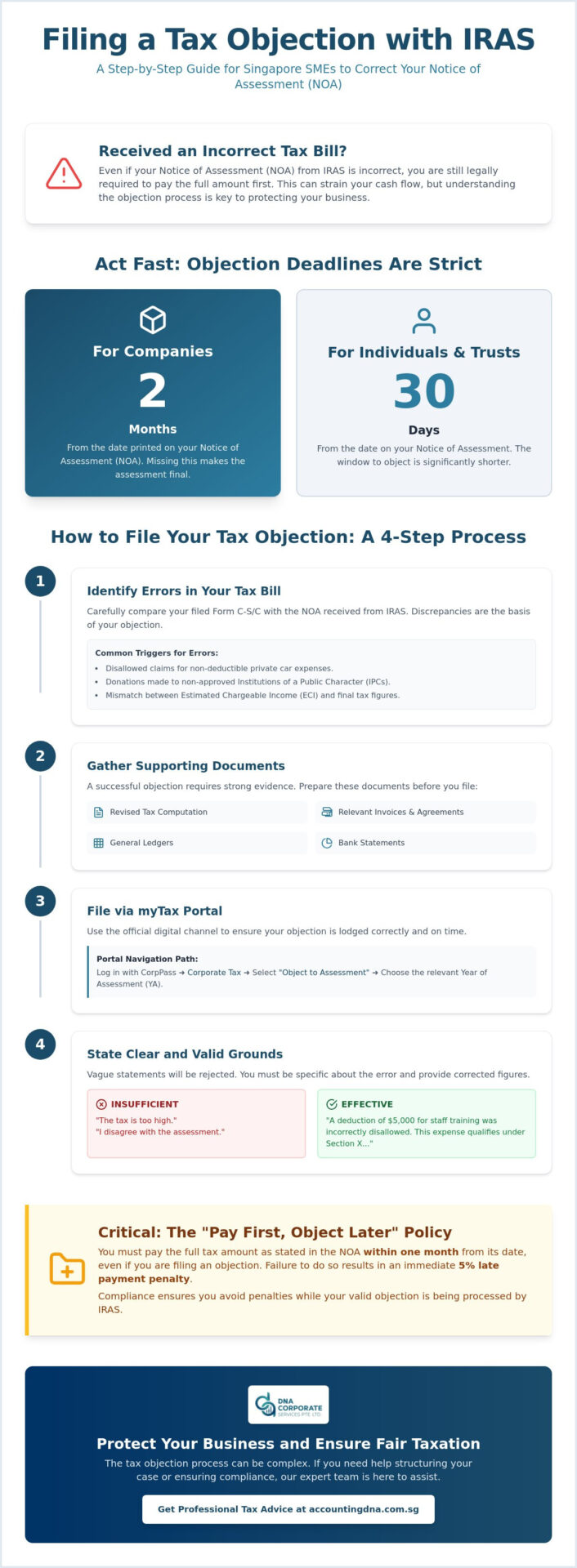

Receiving a Notice of Assessment (NOA) can be a moment of tension for any business owner. This document is the official tax bill issued by the Inland Revenue Authority of Singapore (IRAS), detailing exactly how much corporate tax the Comptroller believes your company owes for the Year of Assessment. While it usually aligns with your filings, discrepancies often arise from adjustments made during the review process. If the figures don’t match your internal records, you need to know how to file a tax objection with IRAS before the window of opportunity closes.

The clock starts ticking immediately. For Singapore companies, you have a strict two-month deadline from the date printed on the NOA to lodge an objection. Individuals and trusts face an even tighter window of just 30 days. If an agreement isn’t reached after your submission, IRAS may issue a “Notice of Refusal to Amend.” This carries significant legal weight; it signals the end of the informal review and requires you to escalate the matter to the Income Tax Board of Review if you still disagree. Managing these timelines is essential to keep your business records clean and your cash flow predictable.

Identifying Errors in Your Corporate Tax Bill

To spot a mistake, place your filed Form C-S or Form C alongside the received NOA. Discrepancies often occur when IRAS disallows certain claims. Common triggers include non-deductible private car expenses, such as S-plated vehicle costs, or donations made to non-approved institutions. We often see cases where the Estimated Chargeable Income (ECI) previously filed doesn’t align with the final figures, leading to unexpected tax liabilities. Reviewing these line items carefully is the first step in understanding how to file a tax objection with IRAS effectively. For professional help with these reconciliations, our taxation services can provide the clarity you need.

The 2-Month Rule for Singapore Companies

Step-by-Step Guide: Filing Your Tax Objection via myTax Portal

Preparation is the foundation of a successful challenge. Before you even log into the portal, you must gather your supporting schedules, general ledgers, and bank statements that prove the discrepancy. If your internal records are disorganized, reaching out for a quick consultation can help you structure your evidence before the deadline passes. Once your documentation is ready, log in to the myTax Portal using your CorpPass credentials to begin the formal process of how to file a tax objection with IRAS.

The most common reason objections fail is a lack of specificity. Writing “the tax is too high” or “I disagree with the assessment” won’t suffice. You must provide clear facts and figures. For example, if you believe a specific deduction for staff training was incorrectly disallowed, your grounds should state the exact dollar amount and why it qualifies under current regulations. This level of detail shows the IRAS officer that your objection is based on merit rather than a simple misunderstanding of the rules.

How to Use the “Object to Assessment” Digital Service

After logging in, navigate to the “Corporate Tax” menu and select the “Object to Assessment” option. You’ll then need to choose the relevant Year of Assessment (YA) from the dropdown list. The “Object to Assessment” service is the primary digital channel for tax disputes in Singapore. This streamlined workflow allows you to input your reasons for objection directly into the system, ensuring your claim is logged immediately within the two-month statutory window.

Supporting Documents You Must Include

Your digital submission is only as strong as its attachments. You must include a revised tax computation that clearly highlights the changes you’re requesting. If you’re claiming capital allowances for new machinery or office equipment, attach the relevant invoices and hire purchase agreements. Ensure all documents are in clear PDF format to avoid delays. IRAS generally reviews objections within six months, and providing organized, legible files from the start can significantly speed up this timeline.

Critical Compliance: The “Pay First” Policy and Avoiding Common Mistakes

Is it possible to delay your tax payment while your objection is being reviewed? The short answer is no. One of the most dangerous misconceptions in Singapore corporate tax is believing that an active dispute pauses your payment obligations. Even if you are currently figuring out how to file a tax objection with IRAS because of a clear error, the law requires you to pay the full amount stated on the Notice of Assessment within one month. This “pay first, object later” policy is non-negotiable. While it might feel frustrating to part with capital for a bill you know is wrong, it’s the only way to protect your business from immediate enforcement actions.

Rest assured that if IRAS reviews your objection and agrees that an overpayment occurred, they’ll process a refund. This typically includes the excess tax paid and, in specific circumstances, interest. However, your priority must always be to keep your company’s compliance record clean while the review, which can take up to six months, is underway. Staying on the right side of the Comptroller ensures your business remains in good standing for future government grants or loan applications.

Avoiding the 5% Late Payment Penalty

Why is the one-month deadline so critical? If the payment doesn’t reach IRAS by the due date, an immediate 5% penalty is slapped onto the outstanding tax. For many SMEs, this is a costly and avoidable mistake. Beyond the fine, IRAS may terminate your GIRO instalment plan, forcing you to settle the entire balance in one lump sum. Our strategic tip is simple: pay the tax first to stop the penalty clock. This allows you to focus entirely on the technical merits of your appeal without the added pressure of mounting fines.

When a Professional Tax Consultant is Essential

Some objections are straightforward, but others involve complex “questions of law” where the interpretation of the Income Tax Act is at stake. If your case escalates to the Income Tax Board of Review (ITBR), having expert representation is no longer optional. Our team provides specialized Corporate Tax & GST Filing Services to help you navigate these high-stakes disputes. We act as your reliable guide, ensuring your arguments are technically sound and your business’s interests are protected at every level of the appeal process.

Take Control of Your Corporate Tax Compliance

Managing a tax dispute doesn’t have to be a source of constant anxiety for your leadership team. By acting within the strict two-month window and adhering to the mandatory “pay first” policy, you safeguard your business from immediate 5% penalties while exercising your legal rights. You now have a clear roadmap for how to file a tax objection with IRAS using the myTax Portal, ensuring your company’s records remain accurate and your cash flow is protected.

Success in these matters lies in the details. Precise grounds for objection and well-organized digital documentation turn a stressful assessment into a manageable administrative task. If the process still feels overwhelming or if your case involves complex interpretations of the Income Tax Act, our team is ready to step in. As experienced Singapore tax consultants, we offer a boutique, SME-focused service designed to provide full ACRA and IRAS compliance support. We pride ourselves on being a protective, flexible partner that understands the unique challenges of the local business landscape.

Get Expert Help with Your IRAS Tax Objection today to ensure your assessment is fair and accurate. Let us handle the technical heavy lifting so you can focus on what matters most; growing your business with confidence.

Frequently Asked Questions

Do I still need to pay my tax bill if I have filed an objection with IRAS?

Yes, you must settle the full amount within one month of the Notice of Assessment date, regardless of your objection status. This is the “pay first, object later” policy enforced by the tax authority. Failing to pay on time triggers an immediate 5% penalty and could lead to the termination of your GIRO plan. Once your objection is successful, IRAS will refund any overpaid tax to your company bank account.

What happens if I miss the 2-month deadline for filing a corporate tax objection?

If you miss the two-month deadline, the tax assessment is usually considered final and conclusive under the Income Tax Act. This means you lose your statutory right to challenge the bill. IRAS only grants extensions in very rare, exceptional cases, such as the company director being hospitalized or away from Singapore for an extended period. It’s vital to track the date on your NOA closely to avoid this outcome.

How long does IRAS take to review a tax objection for an SME?

IRAS generally aims to review objections and provide a decision within six months of receiving complete information. For simpler SME cases, the process might be faster, while complex disputes involving legal interpretations can take longer. You can track the status of your request through the myTax Portal. If you’re unsure about how to file a tax objection with IRAS correctly to avoid delays, providing clear, PDF-formatted supporting documents from the start is the best way to speed up the review.

Can I file a tax objection if I forgot to claim certain business expenses in my initial filing?

Yes, you can certainly file an objection if you discovered missed tax deductions or business expenses after your initial submission. This is a common scenario for many growing businesses. You’ll need to submit a revised tax computation and provide supporting evidence, such as invoices or payment vouchers, to justify the additional claims. Learning how to file a tax objection with IRAS for these omissions ensures your company doesn’t pay more tax than it legally owes.

Disclaimer

The information provided on this website is for general informational purposes only and is not intended to constitute professional accounting, tax, legal, or financial advice. While we strive to ensure that the content is accurate and up to date, regulations in Singapore, including those administered by ACRA, IRAS, CPF Board, and MOM, may change from time to time and may differ depending on individual circumstances.

Readers should not act or rely on any information contained on this website without seeking specific advice from a qualified professional based on their individual situation.

DNA Corporate Services and its affiliates accept no responsibility or liability for any loss or damage arising from reliance on the information provided in this website or any linked materials.

For tailored advice relating to accounting, taxation, corporate secretarial, or compliance matters in Singapore, please contact us directly for professional consultation.